Daily Data: March 5, 2026

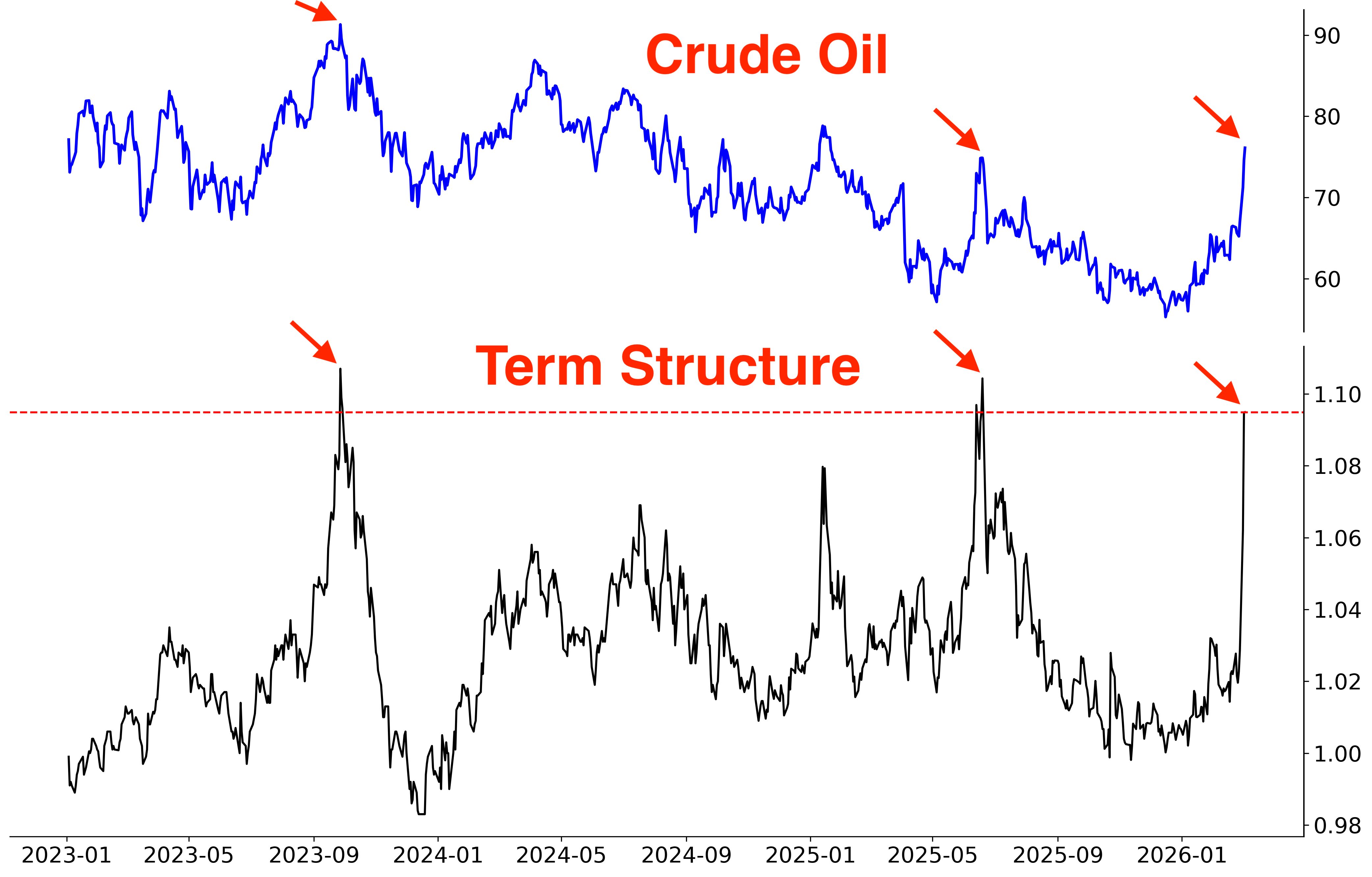

Crude oil term structure

Oil’s term structure is in extreme backwardation. Prior spikes in the past 3 years were topping signs for oil:

Investors’ Intelligence Bulls-Bears

From Matt Cerminaro

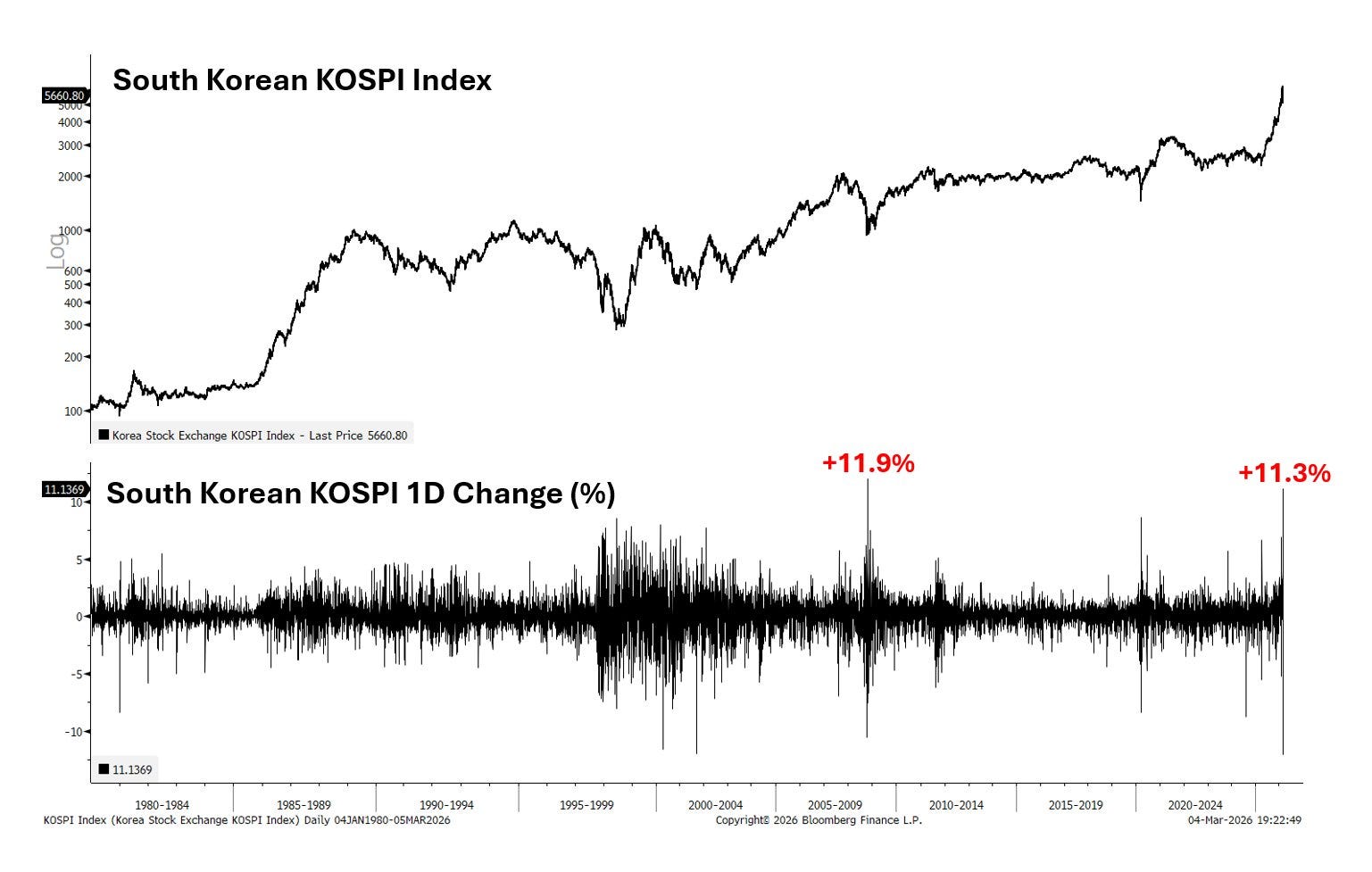

After a big pullback, Korean equities are rallying again.

From Callum Thomas

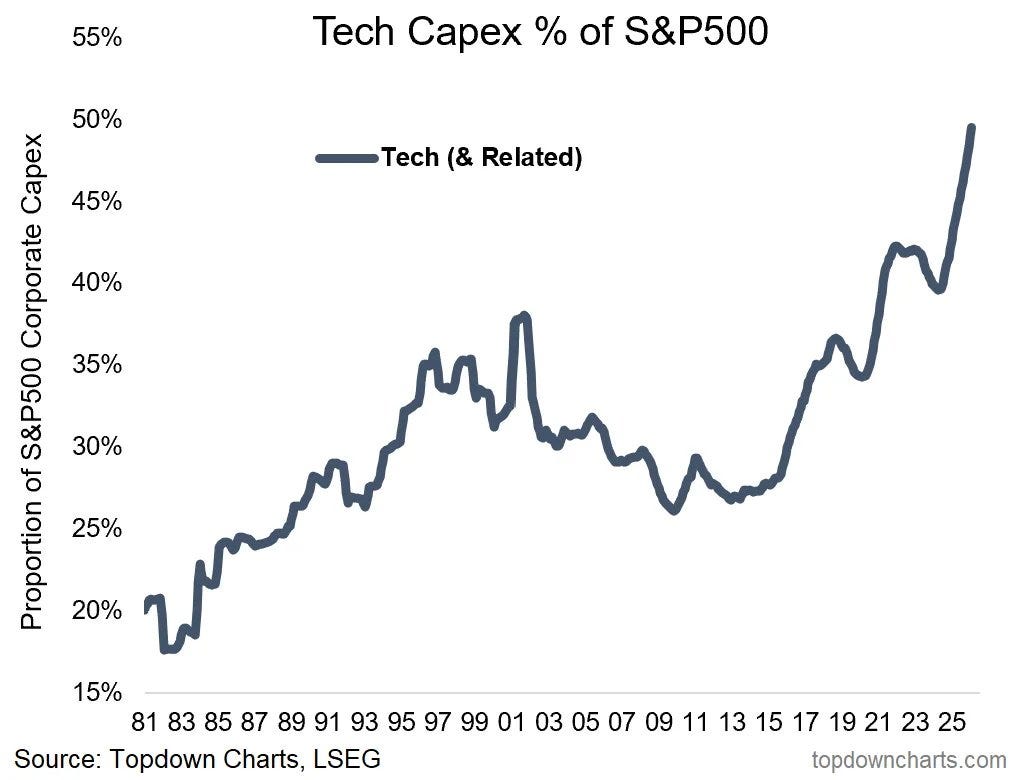

Tech capex accounts for almost half of all S&P 500 capex

From Citadel

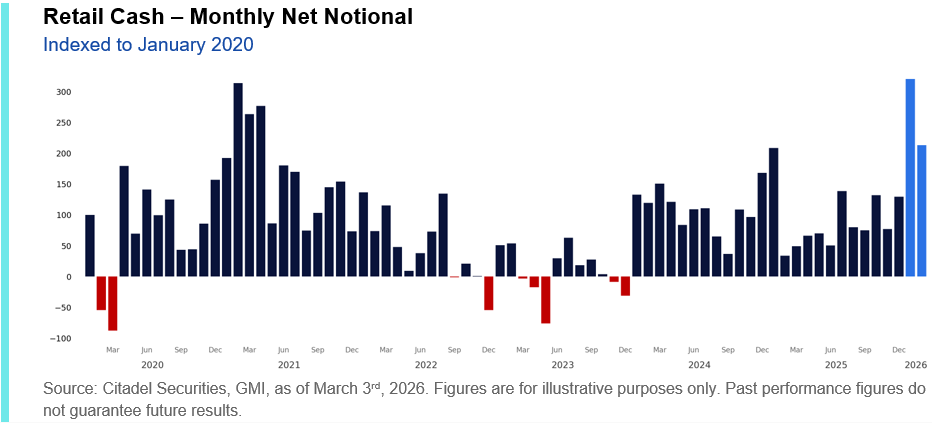

“Retail remains the strongest hand in the entire market. The magnitude and persistence of the buying activity (across both stock and options) has been extremely notable.

As we highlighted a month ago, January 2026 marked the largest net buying month on record on our platform. February flows, while below that January surge, still ranked as the fifth-largest net buying month in our platform’s history and the strongest in ~five years, since April 2021.”

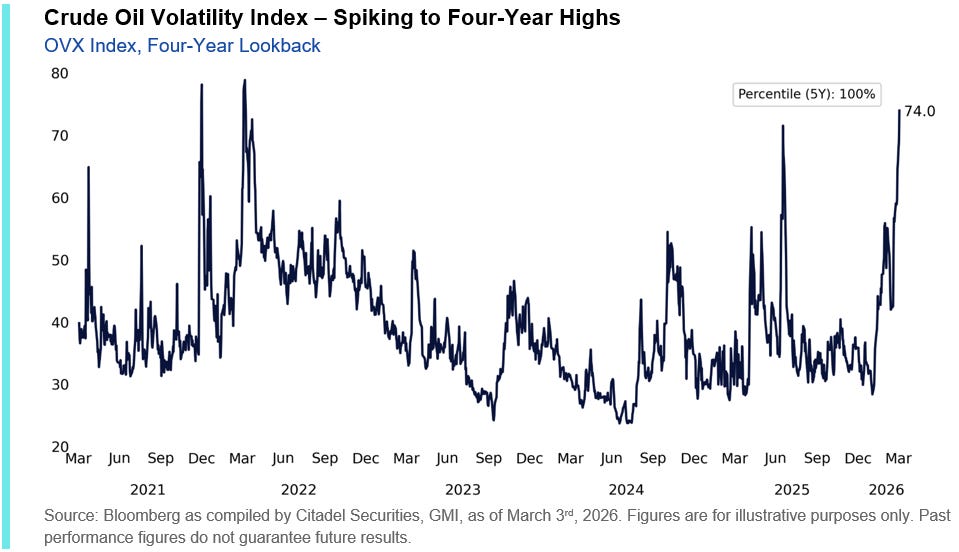

“Amidst increasing geopolitical tensions, crude oil volatility has also severely increased, with OVX (crude oil VIX) spiking back to highs not seen since the beginning of the Russia/Ukraine war (2022).”

Options Flow

Intuit

This flow most likely represents a large institutional synthetic short or hedge on Intuit (INTU) using deep ITM puts. The trader aggressively bought the 700P (2500 contracts) and 600P (750 contracts) at the ask, which behaves almost like shorting stock because deep ITM puts have delta near –1. At the same time, the trader sold smaller amounts of 610P, 590P, 580P, and 550P at the bid, likely to partially finance the expensive deep-ITM purchases. The overall structure suggests a very large bearish positioning or portfolio hedge, likely by a fund protecting or offsetting a large INTU long, using options instead of directly shorting the stock.

ZScaler

This trade appears to be a large institutional synthetic short position in Zscaler (ZS) established using deep ITM puts that expire very soon (Mar 20, 2026). The trader aggressively bought 7,600 contracts of the 270P and 1,075 contracts of the 290P at the ask, paying about $100M in premium, but because these puts are extremely deep ITM and near expiration, almost the entire price is intrinsic value, meaning the options behave almost exactly like shorting stock with delta near −1. In total, the position represents roughly 867,500 shares of synthetic short exposure (~$135M notional). Given the very short time to expiry, this is more consistent with a short-term hedge.

EWY (Korea equities)

2 separate EWY options trades with bullish implications.

In the first trade, a buyer aggressively purchased 5,000 April 17, 2026 $150 calls at the ask, spending about $3.3M to gain upside exposure if EWY rises above $150 from its current level around $134.8, suggesting a bullish near-term view on Korean equities.

In the second trade, a different trader sold 600 January 2027 $125 puts at the bid, collecting roughly $1.2M in premium, which indicates a neutral-to-bullish stance, as the seller benefits if EWY stays above $125 and is effectively willing to own the ETF at a lower price if assigned.

EWZ (Brazil equities)

In the first trade, a trader sold 4,000 December 2027 $30 puts at the bid, collecting about $1.13M in premium, which suggests a neutral-to-bullish stance, as the seller profits if EWZ remains above $30 and is effectively willing to own the ETF at a significantly lower level than the current price around $37.5.

In the second trade, another trader aggressively bought 10,000 May 15, 2026 $41 calls at the ask, paying roughly $1.0M to gain upside exposure if EWZ rises above $41 over the next few months, indicating a bullish bet on a continued rally in Brazilian equities.